The NJ Pension system remains in a fragile state. State (employer) contributions have merely trickled in since Christine Whitman was governor in 1994.

In 1993, the NJ pension system had more than enough assets to cover present and future obligations. But in 1994, then-Governor Whitman proposed a 30% income tax cut, phased in over three years. While tax cuts are popular, keep in mind they create a shortfall somewhere else in the budget. The Whitman administration reduced contributions to the NJ pension system by $3.5 billion over four years.[1]

In 1993, the NJ pension system had more than enough assets to cover present and future obligations. But in 1994, then-Governor Whitman proposed a 30% income tax cut, phased in over three years. While tax cuts are popular, keep in mind they create a shortfall somewhere else in the budget. The Whitman administration reduced contributions to the NJ pension system by $3.5 billion over four years.[1]

At the same time, the state also implemented a new plan where New Jersey would have 60 years to catch up with its earlier under-funding, rather than 40 years. While the state could contribute less in current years (the 1990’s), it meant New Jersey would have to pay more in later years, to catch up.

Their short term problem was fixed. But the long term problem (which they did not anticipate at the time) became life-threatening.

There was only one catch: the state either omitted or contributed very little in the coming two decades. Now the NJ Pension system has fallen far behind. The pension system is now $115 billion behind in payments owed into the system. Whichever way you lean politically, know that both sides are contributors to this mess. Essentially, NJ kicked the can down the road and left the problem of fixing this pension mess to others… namely, me and you.

New Jersey once had a pristine credit rating. Now their debt is massive, problems remain unsolved and the credit rating is among the worst in the nation.

By the way, it’s not just the NJ pension system that has fallen behind. The state is also approximately $35 billion behind in funding for retiree health benefits.

Where is the financial planning lesson for us?

Years back, I had a conversation with a couple where the husband was in sales and worked on commission. He was in the midst of a very bad year in sales and the family was having trouble making ends meet. In order to pay the bills each month, he reduced his tax withholding from his paychecks. At one point he stopped withholding taxes from his paycheck entirely. This solved their problem temporarily. However, about six months later, the family was facing a massive tax bill, plus penalties for underpayment. Paying their tax bill wiped out their reserves. They were considering borrowing against credit cards to make ends meet.

Their short term problem was fixed. But the long term problem (which they did not anticipate at the time) became life-threatening.

What seemed like a short term “patch” over a problem mushroomed into a much larger problem. And the same scenario exists both for this family and also for the NJ pension system.

In a recent video over at Mullooly.net, I discussed a report showing more Americans are skipping vacations this year. They are looking to pay down debt and save money. On a local level, it seems families can spot “leaks” in their cash flow, and they can tidy up their balance sheet when needed. It’s unfortunate that municipalities cannot do the same. There’s often too much pandering and offering favors to gain votes. Tougher decisions (like tightening our belts) get pushed off for another day. Kicking the can down the road does not solve a problem. It only makes the problem go away, temporarily.

And it usually becomes a bigger problem in the future.

Let’s go back to the top of this post: “The NJ Pension system remains in a fragile state. State (employer) contributions have merely trickled in since Christine Whitman was governor in 1994.” But let’s change a few words: Your retirement remains in a fragile state. Your contributions have merely trickled in since Christine Whitman was governor in 1994.

We all know family members and friends who “spend like there is no tomorrow.” There is a “tomorrow.” And you need to be ready to pay for it.

Let’s do something about that. We’d be happy to speak with you about your situation.

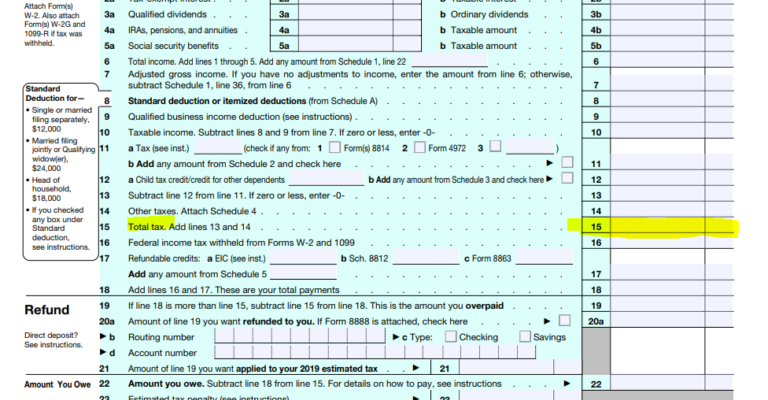

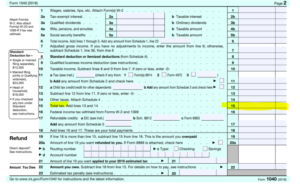

Divide the total tax (the figure on line 15) into line six of your return.

Divide the total tax (the figure on line 15) into line six of your return.