I would like to share a different approach to tax withholding. You may find it helpful. It involves some basic math, but provides a different approach toward withholding for your taxes.

The other day, over on the mother ship (Mullooly Asset Management), I wrote about a tax problem some folks are having. More than a few people are discovering they will receive less than anticipated in a Federal tax refund. Earlier in 2018, the IRS changed the amount each “allowance” is worth. This action lowered the amount many people had withheld from their paycheck throughout 2018.

As a result, many are now learning they will receive a small than expected refund, or possibly owe taxes.

It’s important to know your withholding did not change. And, no one changed the amount of exemptions you claimed. The value of each exemption (allowance) was reduced, and you received more in your paycheck throughout the year.

The problem is many families use that tax refund for vacations, for projects around the home, or a big-ticket item. Although we remind clients all the time, “you’re giving the government an interest-free loan,” many families continue to follow this practice. For some, this is the only way to save money. Sadly.

So here is a different approach to calculating how much to withhold from your paycheck for taxes. The worksheet the IRS provides helps to calculate the number of exemptions (or allowances) to claim. Instead, simply calculate the amount of tax needed, and tell your payroll department to take out precisely that percentage. This works for many people, but will not work for everyone.

STEP ONE

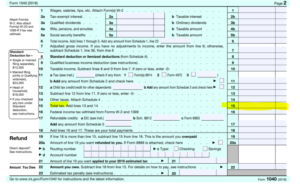

Get out your tax return. The tax form is much more streamlined than in previous years. Jump straight to line 15 “Total Tax.” Note line 15 is not “amount withheld” (which is line 16). You want to know the actual amount of tax owed on the actual amount of income earned. Just grab the total amount of tax owed on your income.

OK, got that number (in dollars)?

Now, take that number and divide it number into the number on line 6. Line six adds up all your income. Do you have additional sources of income, like taxable refunds, alimony, income from a business, capital gains? Include this information as well. Fill out Schedule 1. Carry the information from Schedule 1 over to your Form 1040. This approach works best when you have one source of income, like a W-2 from a single job. It can be modified if you own a business or have varying amounts of gains and losses from investments.

STEP TWO

Divide the total tax (the figure on line 15) into line six of your return.

Divide the total tax (the figure on line 15) into line six of your return.

That number (a percentage) is the actual amount of taxes paid on your income.

It should be a number less than one, for example “0.12657” When rounded, this is thirteen percent. In this case, thirteen percent is the actual tax rate paid on the earnings reported.

Keep this number handy for the next step, as we move on to step three. Step three is where we will match the actual tax (the dollar amount) against the actual dollars withheld. Compare line 15 and line 16 (withholding). Are you getting a refund? Do you owe taxes?

STEP THREE

The percentage of tax paid from step two is important. This number will give you a good “yardstick” to gauge how much to withhold, going forward, as this is your actual tax rate. There is a vast difference between your actual tax rate and your marginal tax bracket (or marginal tax rate). What should you do with this number?

If you owed taxes, this means not enough was withheld from your paycheck. Tell your payroll department to simply increase the percentage withheld for federal taxes. Now you know the rate at which to withhold, from this exercise.

If you received a large refund, you could reduce your tax withholding so it matches the percentage you discovered in step two.

The biggest hurdle for many is dropping the concept of “allowances to claim.” Calculating and claiming allowances is a roundabout way of arriving close to the same numbers. We live in an age where payroll amounts can now be expressed in specific percentages. Tell your payroll area to withhold ___% for Federal taxes (an actual percentage, not a number of allowances/exemptions). Then do the same calculations for your local taxes, too. You can update your Form W-4 with percentages, instead of allowance/exemptions.