The Wall Street extrapolators had a huge miss this week.

The April “jobs report” showed an increase of +266,000 new jobs. This was far below the expectation of one million new jobs. Oops.

The first Friday of each month is “Jobs Day.” This is the day when the Department of Labor releases the unemployment report for the previous month. As we have noted, the report is technically “mid-month to mid-month.”

In this specific May 7, 2021 report, the unemployment report received measured the net job losses and job gains recorded between mid-March to mid-April, 2021.

Leading into the Friday release at 8:30 am, expectations were for one million new jobs added during the period. After all, a similar number (+916,000 new jobs) was reported one month ago in early April.

The Wall Street extrapolators weren’t even close this time around.

And to make matters worse, the +916,000 jobs created in March was revised down to +770,000 upon further review.

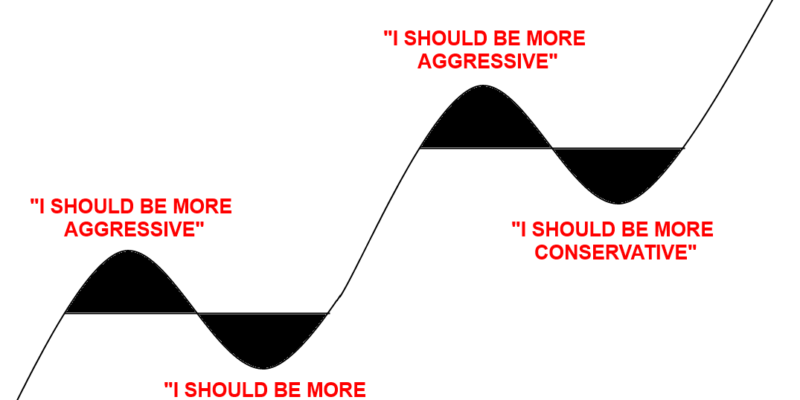

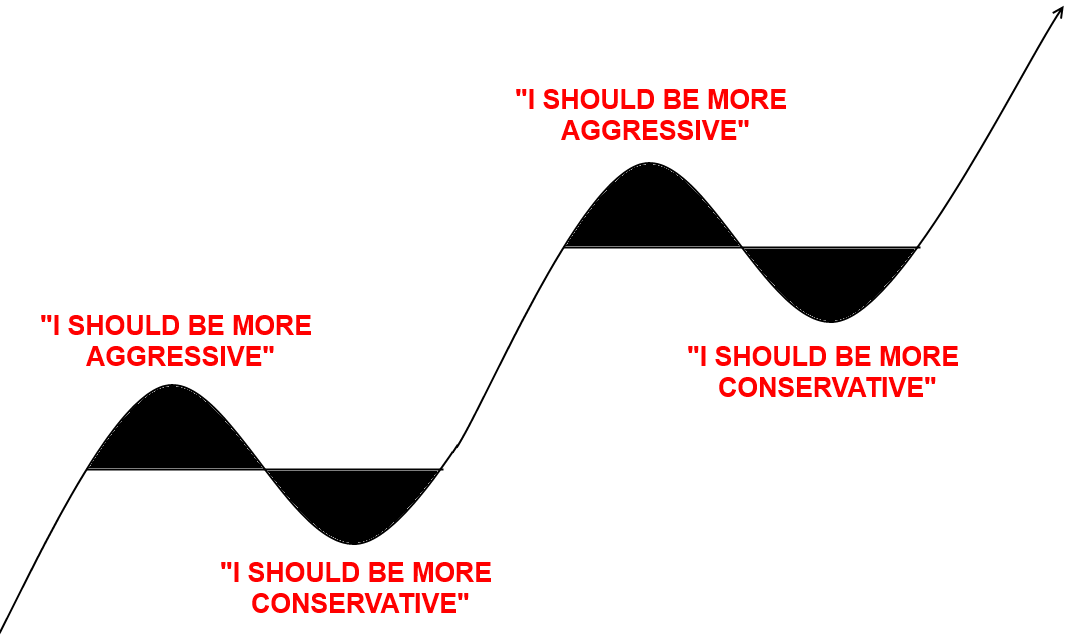

In general, Wall Street loves to extrapolate “one game winning streaks” into “this is exactly how the future is going to be.”

The significant gain in jobs in the March report led to “uncontained glee” in anticipation of how wonderful the April report would turn out. The thinking goes, “if many of the jobs lost last year were now returning, that would lead to wage pressure, which would spur higher inflation.”

Commodities raced ahead in the past few weeks, currencies (listed and unlisted) also pushed higher. This action properly fits with the narrative “the Fed is always behind the curve” and the corollary, “the Fed is often wrong.”

For several months, many on Wall Street have believed that rates must rise sooner than the Federal Reserve has been forecasting. There is some unwritten pressure in the industry to be first, and pressure to be early when it comes to market predictions.

But predictions are often wrong. And since “Wall Street extrapolators” take one data point as “THE new trend” they can often be wrong.

Wall Street extrapolators believe we “must” have inflation.

We’ve been repeating for a long time the Federal Reserve has done an excellent job of communicating with Wall Street and investors. In the past, the Fed was cloaked in secrecy and used circuitous language to remain vague instead of telegraphing their next moves.

Since Alan Greenspan, each successive Fed Chairperson has become more and more clear and straightforward in their communications.

Ben Bernanke was an excellent communicator and had more interviews and question-and-answer opportunities than any Fed chir previously. Janet Yellen (now Treasury Secretary) only improved on Bernanke’s skills. As leaders of the Federal Reserve, Jerome Powell has been the absolute best communicator of all.

Powell and the most recent chairs have been “giving us the answers to the test,” if we would only listen to them. It’s when Wall Street tries too hard to misinterpret the statements when trouble begins.

Powell and other Fed governors have stated many times the “recovery” from the pandemic shutdown will be bumpy and will take time. Results (like new job creation) will take time, one month does not make a trend. At the present time, we are seeing commodities spike higher, because “Wall Street extrapolators” believe we “must” have inflation.

The Fed has not ignored this, and have clearly stated any increase in inflation will be transitory and not permanent. And when asked, the response has been “the Federal Reserve has tools at their disposal to deal with higher inflation if it is not temporary.”

Why does Wall Street seem to have “trust issues” with the Federal Reserve? As we mentioned on the podcast this week, the Fed has done a good job despite the naysayers, and “hasn’t steered us wrong.”