This says it all.

Most folks think precisely the WRONG “next move” —

Volatile Markets are Not Unique

People are worried about volatile markets. At Mullooly Asset, we’ve fielded countless phone calls from investors worried about their investments and concerned about the volatile markets in general.

And most inbound phone calls to us begin with, “So, we’ve never been through anything like this in history…”

Wait. Are you sure?

Perhaps we have been through episodes like this before.

I am just wrapping up a book with stories about people rioting and looting businesses. This book also included tales of people publicly protesting government programs and shortages.

This same book also contained a story about “packing the United States Supreme Court.”

And, amazingly, this book also contains a story about a politician who was declared the winner of his election to the Senate. However, a few days later the decision was overturned when all the votes were counted.

Was it a book about the year 2020?

No. It’s a book chronicling events from eighty years ago!

The book is titled “The Path To Power” and tells the story of Lyndon B. Johnson.

In this first of four books about Johnson, author Robert Caro begin the story of the Johnson family settling in West Texas (“Hill Country”) in the mid-1800’s, right up through Johnson’s campaign for the Senate in 1941.

While “The Path To Power” is a story about one of the prominent political names in the past century, it’s also about events which can lead to turmoil in society and volatile markets.

Protests add to Volatility

In 1931, folks began to realize the volatile markets not just on Wall Street, but in commodity markets were having an impact back home. And following the stock market crash in 1929, local economies were not recovering. And the unfolding economic problems were much longer-lasting than initially perceived.

Jobs were not returning. And times were hard. No one had money. The government had no programs, no money, no assistance to offer. Once proud men and families were left homeless and begging. Children were dropping out of school to work on family farms. Riots, protests and general unrest began taking place on a fairly regular basis in Texas (and elsewhere around the country) throughout 1931 and 1932.

In 1932, Franklin Roosevelt became the first Democrat in 80 years to win the presidency by a majority vote, instead of merely a plurality. On Capitol Hill, House Democrats gained a whopping 97 seats for a nearly three-to-one margin over the Republicans (313 Democrats, 117 Republicans). In the Senate, Democrats picked up 12 seats.

It didn’t end there. In 1934, Democrats picked up 10 more Senate seats for a total of 69. In 1936 that number rose to 76. Over in the House, the Democrats surged to 322 to 103 Republicans, but there were also 3 from the Farmer-Labor Party and 7 from the Progressive Party who often voted Democratic. Republicans held less than 25% of the House by 1936.

Supreme Court Packing can add to Volatility

In 1937, Lyndon Johnson, just 29 years old, ran for Congress in a special election. Johnson’s backers insisted he piggyback on the Roosevelt platform as he began to campaign. The only potential problem was after winning reelection convincingly in 1936, Roosevelt was adamant about packing the Supreme Court in 1937. Roosevelt planned to add six new justices to the Supreme Court.

Similar to some themes heard in 2020, President Roosevelt issued a proposal in February 1937 to provide retirement at full pay for all members of the court over 70. If a justice refused to retire, an “assistant” with full voting rights was to be appointed, thus ensuring Roosevelt a liberal majority.

While Johnson won his seat in the House, most Republicans and many Democrats in Congress opposed his so-called “court-packing” plan. In July 1937, the Senate struck down the plan by a vote of 70 to 22. We did not hear much about “court-packing” again until September, 2020.

An Overturned Election Could Spur Volatile Markets

In 1941, in a special election for a Senate seat, thirty candidates originally threw their hats in the ring. But the votes essentially came down to two people: 32 year old Congressman Lyndon Johnson and Texas Governor “Pappy” Lee O’Daniel.

In 1941, in a special election for a Senate seat, thirty candidates originally threw their hats in the ring. But the votes essentially came down to two people: 32 year old Congressman Lyndon Johnson and Texas Governor “Pappy” Lee O’Daniel.

O’Daniel was a successful businessman, who later became a very popular entertainer. O’Daniel parlayed his popularity into becoming governor. “As one contemporary said, …you couldn’t find anyone who voted for him, but he always won the election.”

On election night, Johnson’s 24 year-old campaign manager, John Connally, asked election officials for their vote tallies. Connally himself had a long career including Secretary of the Navy, Governor of Texas and Secretary of the Treasury, long after managing Johnson’s 1941 campaign.

With 96 percent of the precincts reporting, Johnson was ahead by five thousand votes. Newspapers announced the win for Johnson.

But releasing the vote tallies was a fatal error for Johnson’s campaign. These details gave O’Daniel’s campaign team (and other special interest groups in Texas) the critical information needed to come up with enough “late counted votes” the very next day to beat Johnson by 1311 votes. This was hotly contested for days after the special election date, but eventually Johnson accepted the results.

Can you imagine what kind of volatile markets we might see with a contested election?

Is this something you should be concerned about?

The volatile markets and news headlines we have been experiencing in 2020 may be the first time for some of us. But these kinds of news headlines and stories have happened before.

For the record, we fully expect markets will remain volatile between late October and year-end. For investors (not traders), these weeks of market volatility should not be a reason to “rip up the script” or change your approach with your investments. We’ve put together several videos regarding the markets, the election and volatility which you can find here. Our latest comment on the markets is also found here.

Your emotional strength will be tested. And your patience will be rewarded.

Other sources:

https://www.texasmonthly.com/articles/texas-history-101-8/

https://www.thestoryoftexas.com/discover/artifacts/lyndon-johnson-of-blanco-county

Money Markets Earn Nothing: Now What?

What do you do when the yield on your money market account is essentially zero?

What is a money market fund and what is it for? A money market is a place for you to park short-term cash. That is, cash you’ll need sooner, not later.

The investments inside the money market are not magic. The “ingredients” of a money market fund will likely be very short term Treasury bills. These bills will typically mature within twelve months or less, and many of them sooner than twelve months.

In fact, SEC rules dictate that most of the investments found in a money market fund must mature within 60 to 90 days. If you peek under the hood, it’s also possible you’ll find other financial instruments like bankers acceptances, commercial paper and other notes that come due in ninety days or less.

This is what a friend told me just today:

“I started with a money market at Ally Bank a year ago. I think I was earning 1.4%.

And every month I get an email telling me the yield will be lower. Now I think I am down to 0.3%”

That sounds about right. Take a look at what treasury bills (T-bills) are yielding at the present time. That will give you an indication of what to expect in yield from a money market fund. Right now, as clients have heard us say, “you need a microscope to see a number that small.” As of October 8th, 2020, the current yield on treasury bills coming due in the next three months was 0.09.

You read that right. Oh, and that is the annual return, not the actual return. These yields get updated each business day, here. So, your bank or broker is not “screwing” you. They can only pay what the underlying investments yield, and pass that along to you.

And if you happen to find a money market yielding considerably more than others, do your homework. There is likely a catch.

Additionally, many banks, mutual funds and brokerage firms used to make money on their money market funds. These organizations would charge a management fee, and the fee was typically built in to the cost of the fund. That is not to say you would be charged a fee. Rather, the fee would be assessed on the assets before calculating your return. Many organizations at the present time are foregoing that fee, because the fee would otherwise gobble up the entire return.

Money Market Yields Nothing, Where Do I Invest?

If you like to feel comfortable having cash in the money market, but can’t stand the thought of earning nothing; you’re in a jam. Jason Zweig wrote a post in the Wall Street Journal this week, “Your Cash Earns Zip, Zilch, Nada. Don’t Make It Worse.”

Zweig wrote about some of the returns you may have encountered so far in 2020 if you took your “emergency funds” and invested them in the stock market. It’s not a recommended path. In most cases, the alternatives led to losses. Meaning, not only would you not earn a return, you would have less than you started with. And any interest or dividends earned would not be nearly enough to make you whole. You should pass.

By the way, the panicked folks we see when markets are heading lower are often the people who are “betting the rent.” Almost always, we discover — after the fact — they were investing (better explained, “trading”) money they should never have been trading.

We consistently tell clients at Mullooly Asset Management that cash parked in a money market should be money that will be needed (spent) in the the very near-term. Here are two examples using the “bucket” approach we talk about often with clients:

- If you are actively shopping for a house, that down payment should have been out of harm’s way a long time ago.

- If you have scheduled withdrawals as part of an income plan, the next three-six-twelve months of withdrawals (depending on your risk tolerance) should also be out of the market. Someone relying on that money cannot be taking chances on the market being up when the time comes for a check.

But what about a market crash?

Can’t we just “ride it out” by putting everything in the money market?”

We’ve unfortunately had this conversation more times lately than we care to admit. People are nervous, we understand that. Trashing your personal investment game plan or “ripping up the script” for a general election is a bad move. No matter the outcome, we (the US economy and markets) will go on. Brendan has an excellent post about market returns from Democrats and Republican administrations. Right now the media has done their job. nearly everyone is in a frenzy over this election. Think about that.

When you’re “hiding out” in the money market, you have to be right two times. First, you need to exit at the right point. Then, you need to gauge when to get reinvested. The second step is much harder than the first!

Please heed this message from someone who “tried” doing this several times early in my career. You will be wrong on either the exit or the re-entry. Or wrong on both sides.

And then you will often find yourself asking why you even bothered at all.

How much pain have cost us the evils which have never happened.

-Thomas Jefferson

An almost always better scenario is to “ratchet down the risk.” In other words, do you need to have 100% of your money invested in the market? Or should some portion of your investments go into a different bucket that might go up when the world is upside down? Or some other investment which might provide some alternative — or some income — while we wait for the “growth investments” to recover?

“Moving to cash” or trying to sidestep an event (like an election) is also something that should *never* be done in a taxable account – you will be forking over unnecessary capital gains. It should also *never* be done when paying commissions on trades. But brokers (who get paid on every trade) will never fight you on your decision to sell and buy back — they’ll get paid twice!

Whatever you will need in the short term should be out of the market and in a money market account. Work with a local financial advisor on the Jersey Shore and discuss your risk tolerance, your short and long-range plans and what ought to be invested where.

The nearby photo is what federal agents found in a box spring in Massachusetts and posted to their Twitter account back in 2017. We understand anti-money laundering prevented these folks from depositing it in the bank. At the very least, your money should not be invested here (in the box spring or the mattress).

Election Day 2020

Election Day 2020 is fast approaching.

Election Day 2020 is fast approaching.

I want to stay out of the political maelstrom, and won’t declare my unbridled love for either candidate. But I have not seen too much discussion on one facet of the upcoming election.

There is a possibility we may not know the results of the election for weeks, and possibly longer.

What will happen to markets if this becomes a protracted problem?

We cannot predict the future. But it seems pretty clear to the team here at Mullooly Asset Management to expect volatility before, during and after the week surrounding the election in November.

We fully expect fifty percent of the people who voted in this election will be upset to learn the “other team” won – no matter which side wins.

So we expect bitterness, division, some potential for strife. And possibly violence. And also the potential exists for a contested, drawn-out process where we may not know the results for weeks.

Does all of this change our belief about your investments?

No.

Two points about this election:

First: Six months ago, a terrible virus began running through our communities across the land. We shutdown significant parts of the economy. This shutdown created a “man-made” recession. The stock market slumped quickly, down 35% in just a few weeks as this unpredictable event unfolded right before our eyes.

The virus was an UNKNOWN event.

The upcoming election is a KNOWN event.

Everyone knows when the election will take place. And many people probably know who they will vote for. In fact, for some, all that’s left is the counting.

As with the 2000 election, at some point the results will be known and we can all move forward.

We recorded a podcast recently walking through the tax and revenue platform the Biden campaign has presented. Here is where you can find that podcast and the transcript of that conversation. It will be worth a listen.

Second: The Bush-Gore election in 2000 was also extremely close and disputed. In the end, Bush had 271 electoral college votes, Gore had 266. This was the narrowest of tallies in electoral college history. And like Grover Cleveland in 1888 (and then Clinton in 2016), Gore technically won the popular vote but lost in the Electoral College.

Apparently, the markets did not think much of the disputed election. The S&P 500 closed at 1409 on the day after the election (November 8, 2000), down from closing at 1431 on Election Day, November 7, a drop of 1.5%.

Thirty-five days later, on December 13th, the Supreme Court effectively ended the recount process in Florida. At that point the S&P 500 Index closed at 1360, a drop of 3.4%.

Although those thirty-five days seemed like thirty-five years for me at the time, the world did not end.

In hindsight, electing Gore OR Bush seems pretty tame by today’s yardsticks. Both candidates offered centrist platforms and neither campaign ventured too far to the left or to the right in terms of political promises. And that’s all they offered: promises, from politicians.

Remember, on Election Day 2000, we didn’t know about 9/11, the war in Iraq, or a housing crisis and the “great financial recession” to come.

By contrast, this election seems far more polarizing, doesn’t it? We don’t doubt there will be volatile markets, unrest and disappointment – no matter who emerges victorious.

But we see this “period of unrest” as short-lived. We do not view this “known event” as an episode where we need to change the approach we are using to manage your long term investments.

After the actress Kelly Preston recently passed away, I was speaking with a client about the upcoming election. I pointed out how an unknown event like the virus knocked our economy completely off course. And yet, while damaged and a little bruised, we survived.

However, this election — while controversial — is starting to freak some people out. I said during the conversation, “I believe we can make THIS work.”

And I thought of Preston’s line from “Jerry Maguire,” “…I did the 23 hour Nose route to the top of El Capitan in 18 hours and 23 minutes, I can make THIS work!”

Watch the clip below:

Social Security Decisions

There is no universal answer to social security strategies.

There is no universal answer to social security strategies.

Your situation will be different from your friend or neighbor.

There is no “one-size-fits-all” answer when it comes to social security.

After examining your individual circumstances, we can tell you what we believe is the right answer for your situation.

But you may not like what we have to say.

Coming to the right conclusion for you will depend on several circumstances. These include, but are not limited to, your desire to continue working. Do you need the money? What is your income projection? Are you carrying debt? Are you married or single? How is your health?

Social Security Website

The official social security website (ssa.gov) is an excellent resource. If you have not created your own account, I strongly suggest you do so immediately, at https://www.ssa.gov/myaccount/. Folks can learn a lot from the site, even just by examining their own data which can be found there.

Here are some actual numbers from an individual in her mid-fifties:

- If she decides to take social security at the earliest point in time (age 62) She would receive $2100 per month.

- Her current projected social security benefit at FRA (full retirement age, 67) will be $3100 per month.

- If she can defer taking social security until the latest point in time (age 70), the monthly benefit would be $3900 per month.

Notice the large gap between the decision to take social security at age 62 versus age 67 (considered full, or normal, retirement age). That is a $1000 per month difference, approximately 1/3rd less than the normal distribution a few years later, at age 67.

“But that’s My Money”

Interesting point to share. The individual sharing her documentation with us had $262,700 contributed to social security over her career, so far. Part of that money came from her paycheck, and part from her employers. You can see your own contribution levels on the social security website.

This individual is not ready to retire, she continues to work. Breaking down these numbers, it shows that she has personally contributed $154,029 so far from her paychecks. These are paychecks going all the way back to the 1980’s. And her employers contributed $108,671 over her career.

But go back to what she has paid directly into social security: $154,029. Yes, that is her money. We do not compound because she would have received this money over her career. Using the monthly benefit at her full retirement age of 67 ($3100), she paid in nearly 50 months of benefits. That is $154,029 divided by $3100, or 49.7 months. These are simple illustrations and do not include any cost of living adjustments or take overall inflation into consideration.

In “back of the envelope” terms, her first four years of monthly social security checks are her own money coming back to her. Everything beyond 49 months came from somewhere else. That includes employer contributions, earnings and compounding.

What if she chooses to take the early retirement monthly benefit ($2100) instead? “Her money” winds up being about 73 months, or six years of benefits. The math works out to $154,029 divided by $2100 per month. Think of that as her social security checks received from age 62 through age 68.

Why “35 years of work” matters

These numbers will all change as she continues to work until age 62, age 67 or age 70. Her higher earning years will cancel out the lower-earning years. This includes years where she was home and had no income while her family was growing. What some folks overlook is social security calculates your monthly benefit by looking at your 35 highest earning years.

Think about that. Suppose you began working at age 20 and had social security withheld from your check back then. Now fast-forward to age 52. That income from 1980 is still being factored into your retirement benefit. Your last few years of income (in your fifties and into your sixties) could “cancel” some of the early years of your career when you were probably not earning much.

Unless you played professional baseball or were in the NFL (or both, like this guy), your peak earning years are likely in your fifties, sixties and beyond.

I found a very interesting thread on Twitter the past few days. You may find it helpful what others in our industry are saying. Advisors and planners wrestle over social security decisions all the time.

It’s a discussion we have here with clients…but only on days ending in “y.”

We encourage folks to defer taking social security for as long as they can possibly manage.

- But some simply cannot wait, that is their personal financial situation.

- Some worry about dying early.

- And some worry the money won’t be there.

Some believe the money won’t be there (in the “social security lockbox”). We don’t know the future, but we remain amazed the Government was able to whip up trillions of dollars out of thin air for the virus and the resulting economic shutdown. Some want to defer taking money from their retirement account at work. Even though using the retirement account first, might be a better choice.

So many questions. Speak with your financial planner / investment advisor and get some options mapped out ahead of time.

Here is that Twitter thread:

And another thing about Social Security: People REALLY don’t love it when you say it’s a good idea to delay! One of my readers sends me near-daily emails about why I’m wrong about this. I’m half expecting to find him sitting in my living room some night when I get home. ?

— Christine Benz (@christine_benz) August 21, 2020

Jobs, Jobs, Jobs

Getting a grip on the “Jobs” reports.

We recently referred to news, like unemployment statistics as bad. But without a yardstick, it’s difficult to see if we’re making progress. Let’s decipher the jobs data we’ve been seeing the last few months.

Initial Jobless Claims

Every Thursday morning (at 8:30 ET) we get the “initial jobless claims.” This is a report showing us how many people filed for unemployment for the very first time. This is the first filing after losing jobs via furlough, temporary layoffs or permanent layoffs. When the shutdown began in March, and people began losing jobs, the initial jobless claims were enormous.

Through late March and into April, more people lost jobs. The initial jobless claims spiked to more than six million. These initial (first-time) claims have steadily shrunk since then. Throughout May and June we still heard stories of folks around the country, still without jobs. Even right here in Monmouth County, NJ, many had trouble reaching the local unemployment office.

The initial claims continue to stream in, but at a slower pace each week. Data released Thursday August 6th, 2020 showed a decrease in first-time claims from the previous week of 249,000 claims. In total last week 1.2 million initial jobless claims were processed. These remain historically high numbers.

Continuing Claims

Continuing claims have taken on more relevance lately. These numbers are also reported each week, on Thursday morning at 8:30am. Continuing claims are the number of individual remaining on unemployment, still looking for jobs. A little bit of algebra gives us the numbers returning to work. Continuing claims are always two weeks behind. Data reported on August 6th represents continuing claims from the week ending Saturday July 25th.

This week, continuing claims are 16,107,000. This is a drop of 844,000 from the prior week’s report. This can be interpreted as 844,000 people returned to work. This is still a gigantic number of folks not working.

The Unemployment Report

On the first Friday of each month, we get the “unemployment report” from the Department of Labor. This report will give us the overall unemployment rate.

The unemployment rate for June, reported in July was 11.1%.

The unemployment rate for July, reported Friday August 7th, was 10.2%.

Technically, this “unemployment rate” is called the “U3 report.” That’s important to know because there are other reports examined each month. These include the U5 and U6.

There is one bit of nuance many miss is when we refer to the “unemployment rate.” This report measures the period from mid-month to mid-month, not calendar months. The July unemployment report measures employment data from mid-June to mid-July.

What if there are any significant changes occurring late in a month? That may not be accurately reflected in the current numbers.

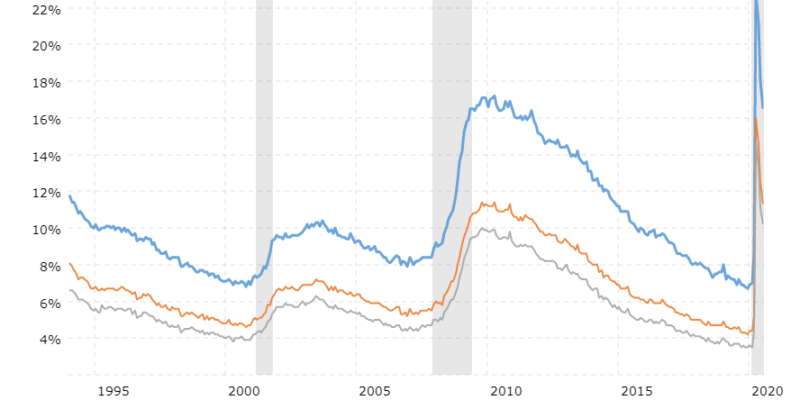

More on U3, U5 and U6

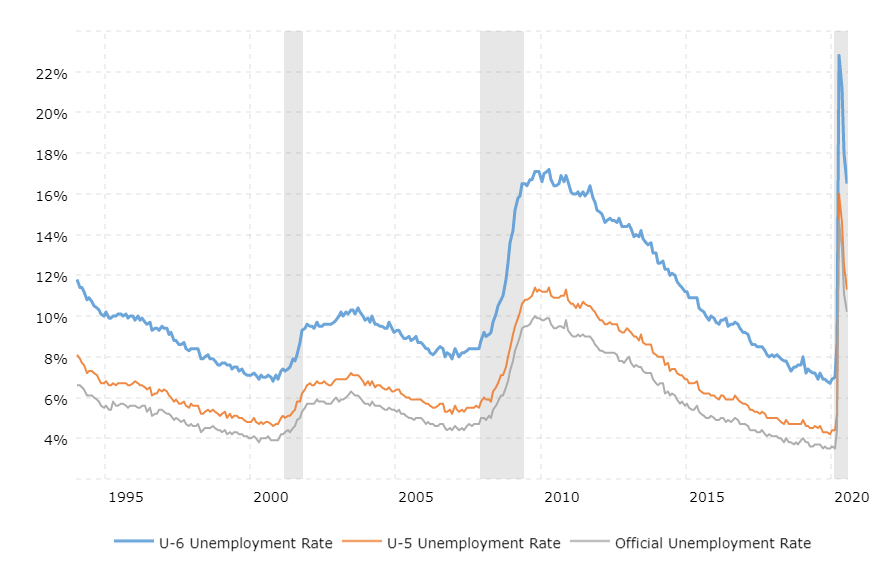

Two other data points released on the first Friday each month are the U5 and U6 reports. The chart nearby, courtesy of Macrotrends, displays the U3, U5 and U6 data points, going back to the mid-1990’s. The grey bars represent recessions.

The U5 report also includes discouraged workers and all other marginally affected workers. This number represents people who have stopped looking for jobs, but would like to work.

The U-6 number is the total number of unemployed people without jobs. The U6 report includes individuals working part-time purely for economic reasons. This measures the number of folks working part-time but want to work full-time. The current U-6 reading is 16.5% This is a “depression-size” number. Last month (June 2020), the U-6 number was 18.0%

The Street.com also put together a good primer on unemployment statistics which you can see here.

If you’ve never seen Mel Brooks’ “History of the World, Part I” there is a great scene regarding unemployment and jobs. Bea Arthur (from “Maude”) as always, does her very best deadpan: