“Inflation will return, you’ll see.”

Since the Federal Reserve took action to spur the economy, nearly everyone has predicted the return of inflation. The prospects of inflation helped drive oil prices higher, in some ways sparked the commodity boom in 2011, and has otherwise kept market pundits scratching their heads wondering when runaway inflation will return.

The Federal Reserve lowered interest rates to zero. But lowering rates to zero wasn’t enough to get the economy moving. And moving to “negative interest rates” was not under consideration. Negative interest rates now exist throughout Europe, with lackluster results.

One key difference with the recession of 2007-2009 (when compared with other recessions) was that many banks had technically failed in the 2007-09 recession. We say “technically” because while bank branches remained open, very little “banking business” (lending) was taking place. After changing accounting rules (mark to market accounting) during the first week of March 2009, banks, and the stock market came roaring back).

So, moving the goal posts helped get the market moving. We wrote about “mark to market” here, here and also here. But how to get the economy moving?

The world revolves on credit.

With rates already at zero, the Federal Reserve began a program of “Quantitative Easing.” This was a method for the Fed to continue adding liquidity to the system without being able to lower rates. The Federal Reserve began draining the banking system of bonds. Not only Treasury bonds, but also some corporate bonds too. When the Federal Reserve buys bonds in the open market, they are removing “inventory” from the marketplace. Think about what happens when you are shopping. When someone buys (makes a purchase), they are handing over cash to the seller. By draining the banking system of bonds, they were putting cash into the banks. Clever.

And the Federal Reserve wasn’t messing around. They initiated several rounds of “QE” in an effort to get the US economy moving.

“Won’t we have high inflation if the banking system is flooded with cash?” The underlying concept being if the central bank floods the system with too much cash, this will cause inflation. And QE was a massive project.

Many expected inflation.

But it has not materialized, even after ten years. Why?

Well, here’s one big reason. While the Fed was pumping money into the banks, it was also offering the banks a risk-free opportunity. They offered all banks the ability to earn interest on excess reserves. So the banks would take in cash from the bond sales, and keep the cash they needed to create enough loans. Lending is how banks make money. The “excess” would be returned to the Federal Reserve (the “banker for the banks”) where they would earn a risk-free return. At the height of the recession tension (in late 2008), the Federal Reserve was paying banks 1.00% interest on excess reserves. IN March 2009, the Federal Reserve set the rate for interest on excess reserves to 0.25%. Not much, but it was a positive return for banks instead of risking the money out in loans.

The Fed kept the rate for interest on excess reserves at 0.25% until January 2016, when it raised that rate to 0.50%. While Quantitative Easing scared many market pundits with the potential for inflation, the Fed offered a way for banks to work smartly and keep things moving along.

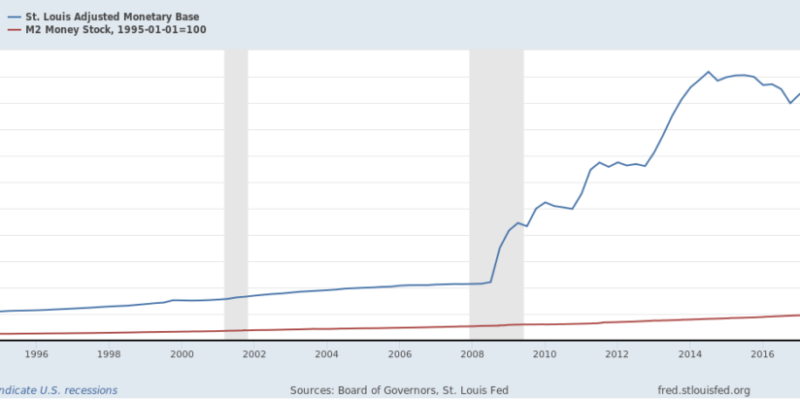

Check out the chart (below) from the St. Louis Fed (a fantastic website): the blue line, which essentially starts to blow up in late 2008 represents the “adjusted monetary base” in the banking system. The red (steady) line represents the growth of M2. M2 is often used as a yardstick to measure money supply in the system. And M2 helps gauge future inflation.

It’s important to understand how inflation gets measured. Printing money does not automatically imply inflation lies ahead.